TL;DR

- Steady U.S. issuance: 47 offerings raised $20.1B in April, with 14 IPOs ($10.2B) and 33 follow-ons ($9.9B).

- IPO comeback: April’s 14 priced IPOs marked the highest monthly count since November 2021, with a +20.6% dollar-weighted 1-day return.

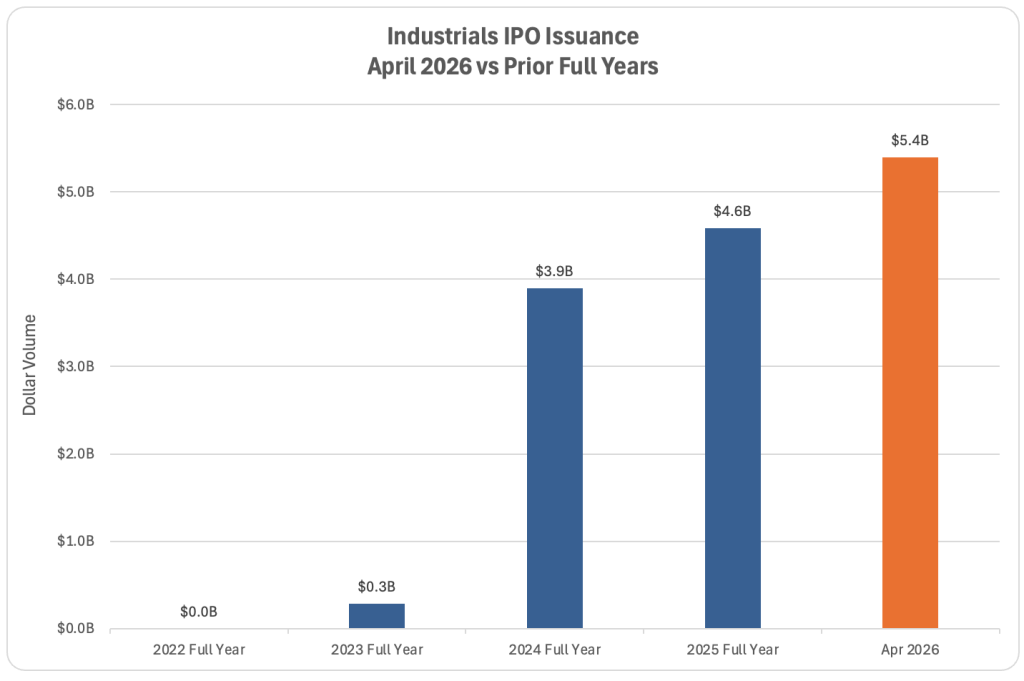

- Industrials in focus: The sector drove 52.8% of IPO proceeds ($5.4B across 5 deals) – a single-month total that exceeds full-year Industrials IPO issuance in each of the prior four years. Industrials also led all-offering-type performance with +21.8% 1-day and +30.9% 3-day dollar-weighted returns.

- Energy cools sharply: After flagging the week ending April 3 as Energy’s busiest week since January 2017, the sector finished the month with just 2 offerings, down 84.6% MoM from March’s 13.

- Healthcare leads by count: 24 offerings raised $7.6B, the most active sector in April across all offering types.

- Cornerstone backing strengthens: 9 cornerstone-backed offerings raised $6.6B with $1.7B (~26%) attributable to cornerstone commitments and delivered a +26.5% 1-day dollar-weighted return – a meaningful signal of institutional demand.

U.S. ECM Holds Its Footing as IPO Engine Restarts

U.S. equity capital markets activity in April was defined by a long-awaited reawakening of the IPO calendar. 47 offerings raised $20.1B, split between 14 IPOs at $10.2B and 33 follow-ons at $9.9B. The standout figure: April’s IPO count was the highest in a single month since November 2021, when 23 offerings greater than $50M priced. IPOs also delivered a +20.6% dollar-weighted 1-day return – a result that should reinforce issuer confidence and pricing power into May.

Sector Spotlight: Industrials Stage a Breakout

Industrials emerged as April’s defining narrative. The sector accounted for 52.8% of IPO issuance – 5 offerings raised $5.4B +25.8% 1-day dollar-weighted return. For context, $5.4B in a single month exceeds full-year U.S. Industrials IPO issuance in each of the last four years.

Industrials across all offering types – the strongest sector across the curve:

- 1-day: +21.8%

- 3-day: +30.9%

- 7-day: +28.5%

Energy: From Multi-Year High to Sharp Reset

In our weekly commentary, we flagged the week ending April 3 as Energy’s busiest week since January 2017. That early-month strength did not carry. Energy issuance fell to just 2 offerings in April, an 84.6% decline from March’s 13. The reversal is worth watching: sponsors and operators appear to have front-loaded monetization into favorable conditions earlier in the year, and the deceleration may signal that secondary supply has calmed for now.

Healthcare: The Quiet Heavyweight

Healthcare retained its position as the most active U.S. sector, with 24 offerings raising $7.6B across all offering types. The sector continues to provide consistent breadth even when sector-specific narratives (Industrials, Technology) capture headlines.

Cornerstone Investment: A Quiet Tailwind

A theme worth flagging for syndicate desks: 9 of April’s offerings were cornerstone-backed, collectively raising $6.6B with $1.7B (~26%) attributable to cornerstone commitments. Those deals printed a +26.5% dollar-weighted 1-day return, above the IPO and broader market averages.

Looking Ahead

With 7 US IPOs already priced in May and 4 more on the road, the calendar is set up for a constructive multi-month IPO stretch.

For weekly ECM commentary and monthly, quarterly and annual recaps, follow CMG’s LinkedIn page.