TL;DR

- Stable U.S. issuance: November raised $18.8B across 58 deals, with IPOs delivering +18.8% day-1 performance and follow-ons adding $16.4B at a 6% discount.

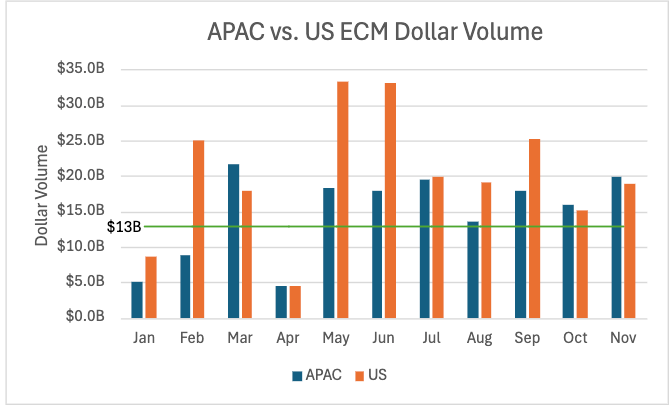

- APAC momentum: The region logged its seventh straight month above $13B, a run last seen in 2021.

- LATAM rebound: $2.9B across 5 deals marked its strongest month since July 2024, ending a three-month stretch with no offerings greater than $50M.

- Healthcare leads again: 28 deals raised $5.6B, its third consecutive month as the top U.S. sector and third straight month above $5B, with +8.4% dollar-weighted day-1 returns.

- Lock-ups ahead: 50 expirations arriving in December, nearly half in Healthcare, set the stage for elevated secondary supply into year-end.

Steady U.S issuance levels

U.S. markets in November remained stable, with $18.8B raised across 58 offerings. Of these, 7 IPOs represented $2.4B in proceeds and delivered strong aftermarket performance, averaging +18.8% day-1 returns. The 51 follow-ons contributed the remaining $16.4B, pricing at an average 6% file-to-offer discount.

A global look: Shifts in international activity

While U.S. issuance demonstrated steady momentum into year-end, APAC continued to stand out, recording its seventh consecutive month of $13B+ in issuance—a streak last observed in 2021.

LATAM also deserves recognition after delivering a sharp rebound, posting $2.9B across 5 offerings, marking its strongest month since July 2024. This performance effectively ended the region’s three-month stretch with zero offerings greater than $50M, underscoring renewed appetite for capital deployment.

Sector spotlight: Healthcare dominance continues

Healthcare once again led U.S. issuance with 28 offerings raising $5.6B, marking:

- The third consecutive month in which Healthcare was the most active U.S. sector.

- The third straight month of $5B+ raised, a trend last seen during the period of January – March 2024.

- A dollar-weighted one-day return of +8.4%, outperforming all other sectors.

For weekly ECM commentary and monthly, quarterly, and annual recaps, follow CMG’s LinkedIn page. As noted in our October report, we flagged the upcoming lock-up expiration for notable outperformer Hinge Health (+40.1%). Following its lock-up expiration, Hinge Health (HNGE) priced two secondary blocks in November totaling $189M, further contributing to sector activity.

Lock-ups ahead

Looking ahead, 50 lock-ups are set to expire in December, with nearly half tied to Healthcare, positioning the sector for continued secondary flow into year-end.